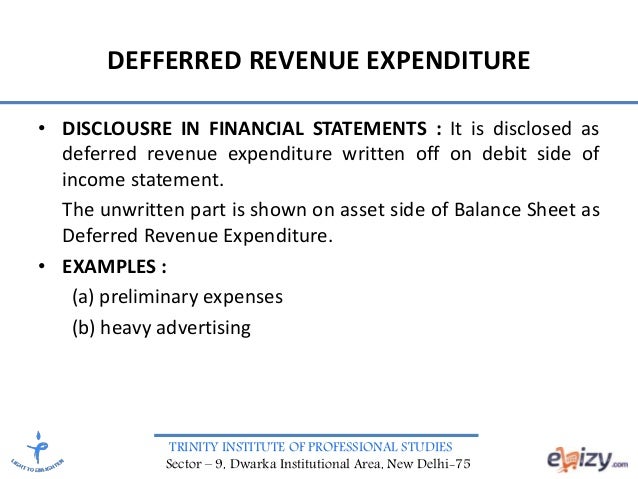

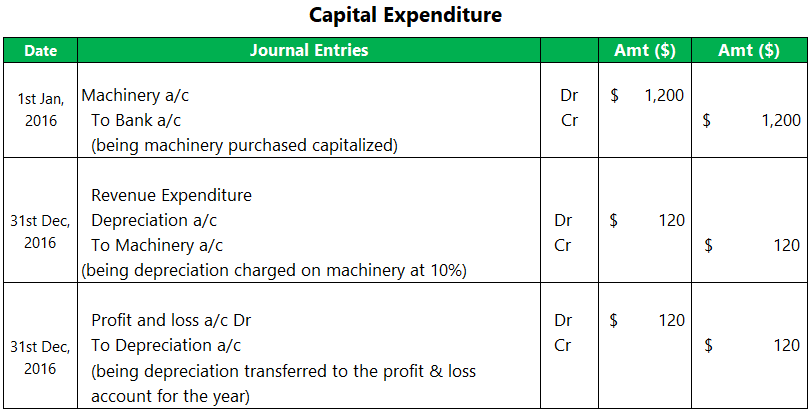

Deferred Revenue Expenditure Journal Entry Example

Deferred Revenue Examples Journal Entry In Accounting Youtube

Deferred Revenue Journal Entry Double Entry Bookkeeping

How To Record Deferred Revenue Accounting Education

Deferred Revenue Expenditure Definition Examples

What Is Deferred Revenue Expenditure Youtube

Deferred Revenue Expenditure Examples Of Thesis Unyrxg Syuapegil Info

In business deferred revenue expenditure is an expense which is incurred while accounting period.

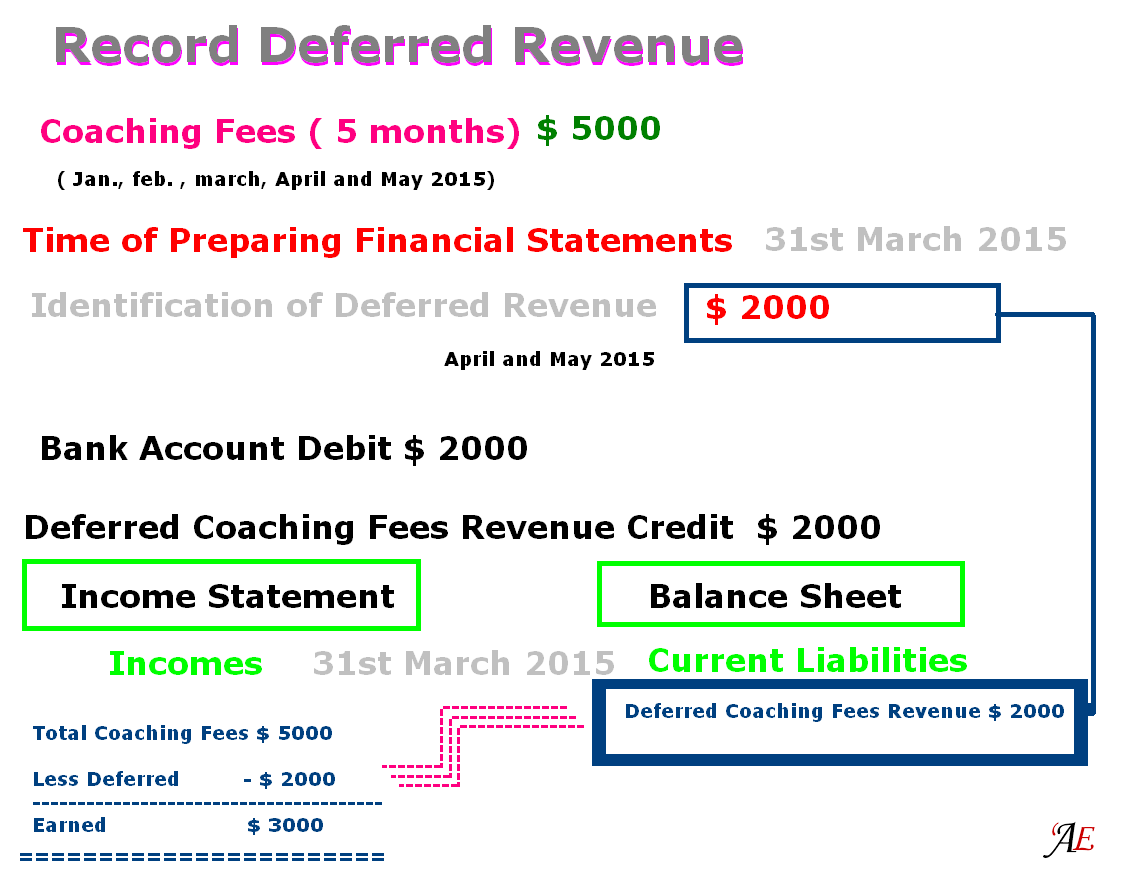

Deferred revenue expenditure journal entry example. Suppose company a has sold software to another company b and received the subscription fees for the same of 100 000 per year for the next 5 yrs. Record the earned revenue. It will be easier to understand the meaning of deferred revenue expenditure if you know the word deferred which means holding something back for a later time or postpone. Accrued revenue and expenditure journals revenue.

To do this your accountants will make the following deferred revenue journal entry. It is the revenue that the company has not earned yet. Deferred revenue journal entry overview. Deferred revenue is the payment the company received for the goods or services that it has yet to deliver or perform.

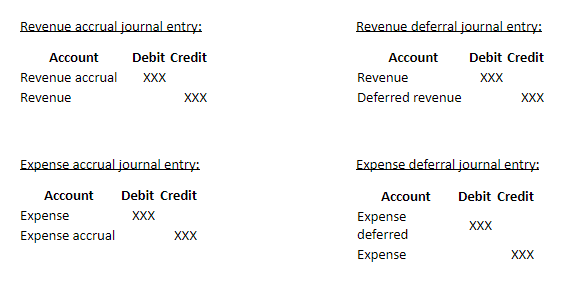

And the result and benefits of this expenditure are obtained over the multiple years in the future. Deferred revenue expenditure is an expenditure which is revenue in nature and incurred during an accounting period however related benefits are to be derived in multiple future. At this stage you will need to update the journal entry in the previous step by reducing the balance sheet liability and transferring the amount to the income statement. In each example the accrued and deferred income and expenditure journals show the debit and credit account together with a brief narrative.

The following are examples of the deferred revenue journal entry. For a fuller explanation of accrued and deferred income and expenditure journals view our accruals and deferrals tutorial. For the next two months the expenditure of inr 20000 made will serve as an asset to the student as it is providing him with benefits. For example revenue used for advertisement is deferred revenue expenditure because it will keep showing its benefits over the period of two to three years.

Examples of deferred revenue journal entry.

Accruals And Deferrals Double Entry Bookkeeping

Deferred Revenue Understand Deferred Revenues In Accounting

Deferred Tax Asset Journal Entry How To Recognize

Deferred Revenues Cash Is Received Before Revenue Is Recognized Slides 1 11 Youtube

Revenue Expenditure Top 3 Examples Of Revenue Expenditure

Adjusting Entries Double Entry Bookkeeping

Accruals And Deferrals Bookstime

What Is Deferred Revenue Expenditure Accountingcapital

Deferred Revenues Odoo 14 0 Documentation

What Are Adjusting Journal Entries

Expense Journal Entries How To Pass Journal Entries For Expenses

What Is Revenue Expenditure Accountingcapital

Incorporation Expenses Double Entry Bookkeeping