How To Reduce Revenue Journal Entry

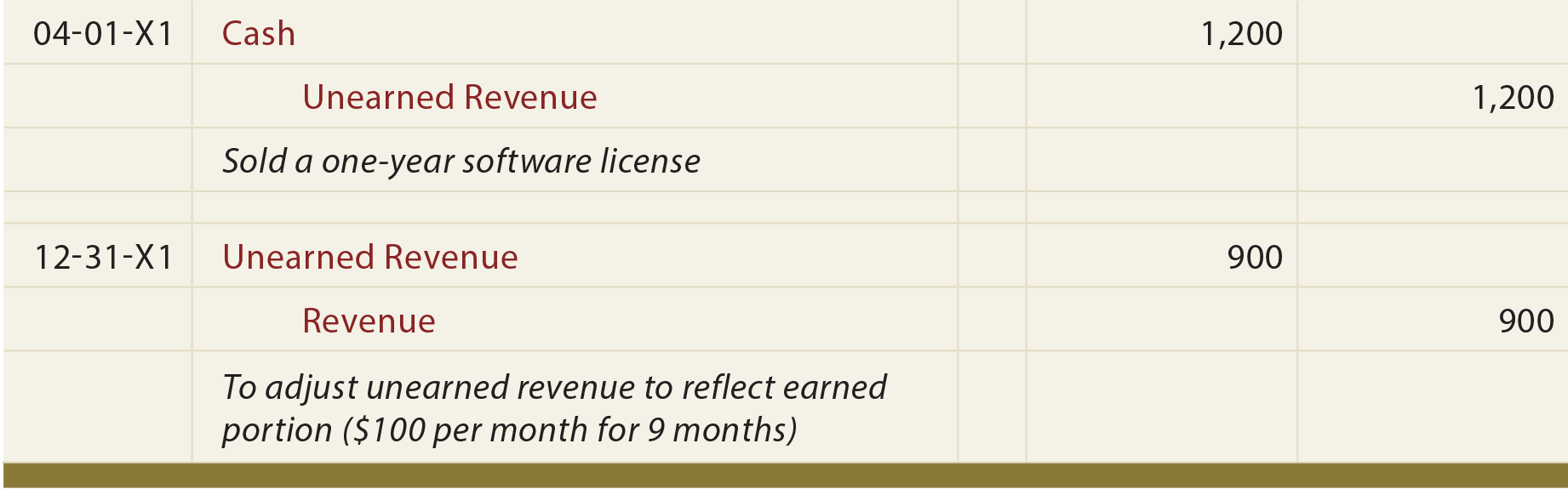

Deferred Revenue Journal Entry Double Entry Bookkeeping

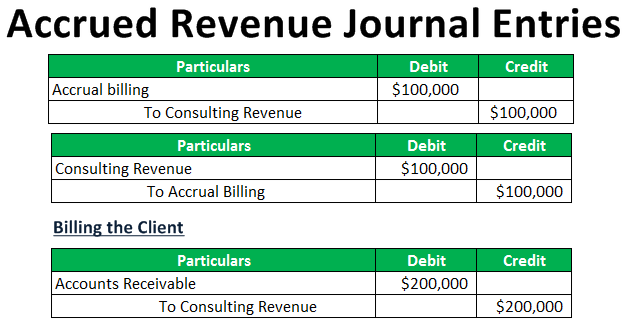

Accrued Revenue Journal Entries Step By Step Guide

The Adjusting Process And Related Entries Principlesofaccounting Com

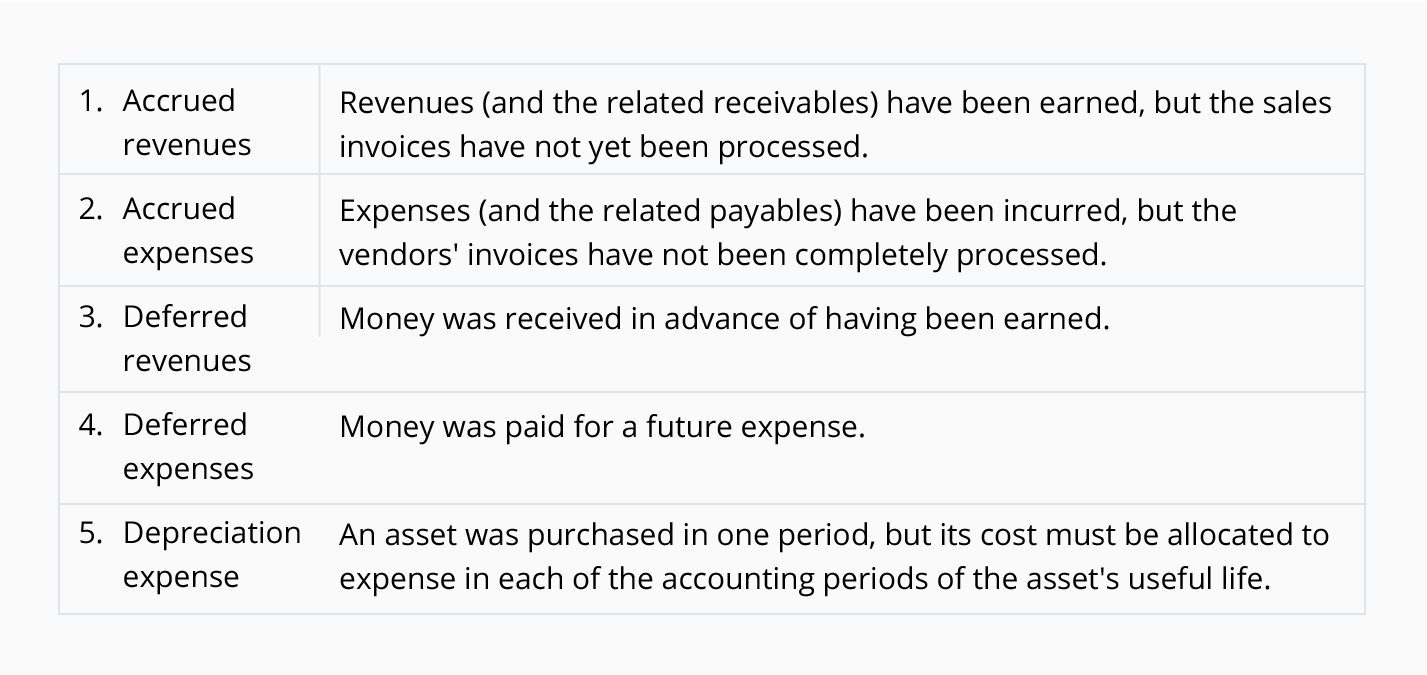

What Are Adjusting Journal Entries

Record And Post The Common Types Of Adjusting Entries Principles Of Accounting Volume 1 Financial Accounting

Accounting For The Billing Cycle

The amounts on the provisional project revenue and revenue coverage accounts are always the same.

How to reduce revenue journal entry. Consider the following diagram. Accrued revenue is the income that is recognized by the seller but not billed to the customer. The recordation of a sales tax liability. In simple terms deferred revenue means the revenue that has not yet been earned by the products services are delivered to the customer and is receivable from the same.

Adjusting entry for accrued revenue accrued income or accrued revenue refers to income already earned but has not yet been collected. Adjusting journal entries are a feature of accrual accounting as a result of revenue recognition and matching principles. A deferred revenue journal entry is needed when a business supplies its services to a customer and the services are invoiced in advance. A journal entry is simply a summary of the debits and credits of the transaction entry to the journal.

More examples of journal entries accounting equation double entry recording of accounting transactions debit accounts credit accounts asset accounts liability accounts equity accounts revenue accounts expense accounts. What is journal entry. An adjusting journal entry is usually made at the end of an accounting period to recognize an income or expense in the period that it is incurred. Basics of journal entries accounting journal entry examples.

This means that the debtors to provisional project revenue vat entry replaces the debtors to revenue vat entry that is created if work in progress entries are not used. Adjusting journal entries. At the end of every period accountants should make sure that they are properly included as income with a corresponding receivable. What are adjusting journal entries.

The purpose of adjusting entries is to ensure that all revenue and expenses from the period are recorded. This journal entry needs to record three events which are. The recordation of a sale. It is treated as an asset in the balance sheet and it is normal in every business.

A sales journal entry records the revenue generated by the sale of goods or services. Journalise a project revenue entry. Many adjusting entries deal with balances from the balance sheet typically assets and liabilities that must be. You ll notice the above diagram shows the first step as source documents.

The recordation of a reduction in the inventory that has been sold to the customer. Journal entry for accrued revenue. Journal entries are important because they allow us to sort our transactions into manageable data. The content of the entry differs depending on whether the customer paid with cash or was.

The following deferred revenue journal entry provides an outline of the most common journal entries in accounting. The matching principle states expenses must be matched with the revenue generated during the period.

Unearned Revenue Definition Explanation Journal Entries And Examples Accounting For Management

Accounting Basics Revenues And Expenses Accountingcoach

Accrued Revenues

Use Journal Entries To Record Transactions And Post To T Accounts Principles Of Accounting Volume 1 Financial Accounting

Explain The Revenue Recognition Principle And How It Relates To Current And Future Sales And Purchase Transactions Principles Of Accounting Volume 1 Financial Accounting

Accrued Income Tax Double Entry Bookkeeping

Account For Uncollectible Accounts Using The Balance Sheet And Income Statement Approaches Principles Of Accounting Volume 1 Financial Accounting

Expense Journal Entries How To Pass Journal Entries For Expenses

Deferred Tax Asset Journal Entry How To Recognize

What Is Unearned Revenue A Definition And Examples For Small Businesses

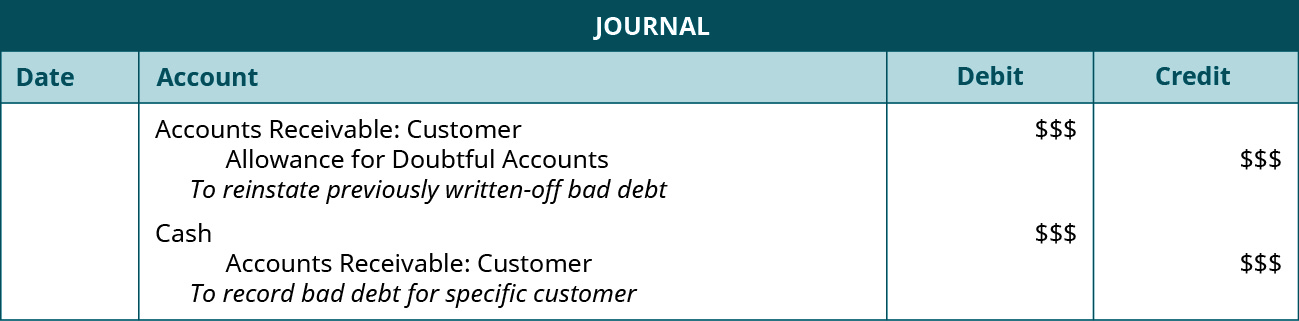

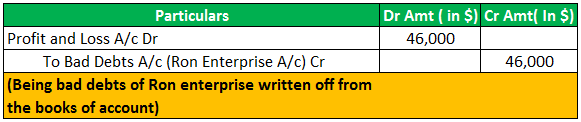

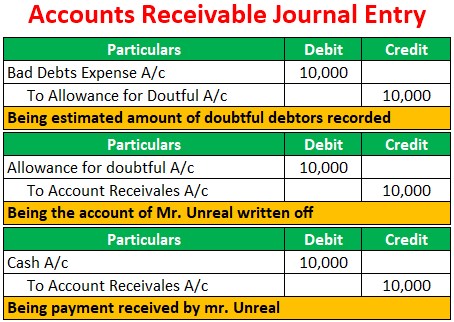

Accounts Receivable Journal Entries Examples Bad Debt Allowance

Bookkeeping Adjusting Entries Reversing Entries Accountingcoach

Bad Debt Overview Example Bad Debt Expense Journal Entries