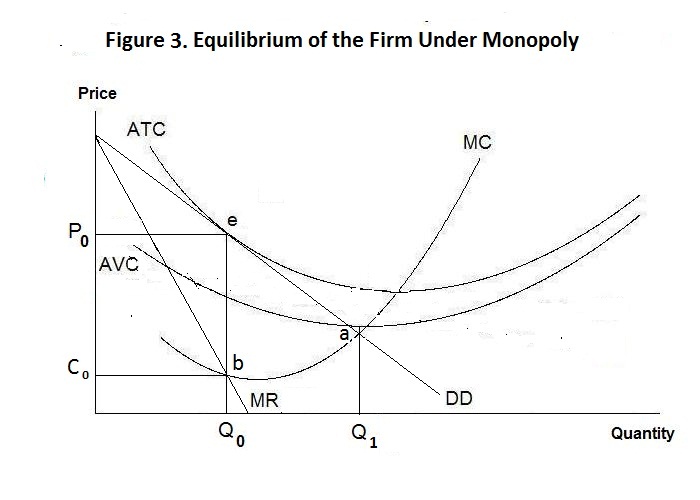

Marginal Revenue Equals Average Total Cost

The Firm Under Competition And Monopoly

Pin On Eco Mate Estadistica

Reading Profits And Losses With The Average Cost Curve Microeconomics

Marginal Revenue Definition Example And Formula Boycewire

Pin On Ideas

Reading Choosing Price And Quantity Microeconomics

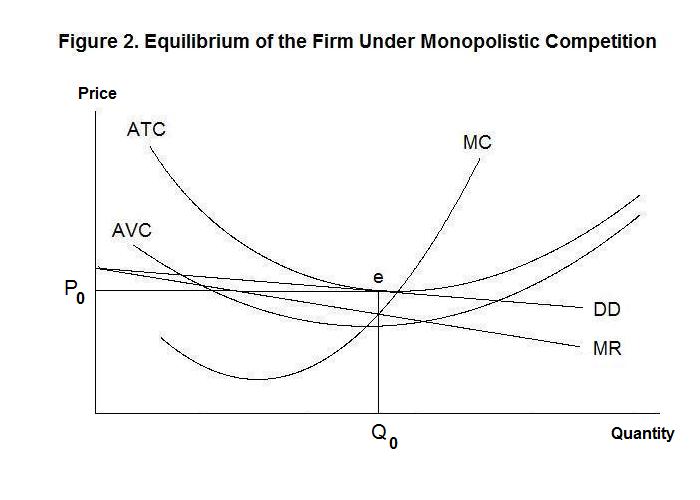

And should decrease its quantity supplied until marginal revenue equals the marginal cost of production.

Marginal revenue equals average total cost. At the production of 4th unit marginal cost and average cost are equal. The revenue concepts commonly used in economic are total revenue average revenue and marginal revenue. In the same fashion average revenue and marginal revenue can also be calculated from total revenue. The average cost of producing 100 units is 2 or 200 100.

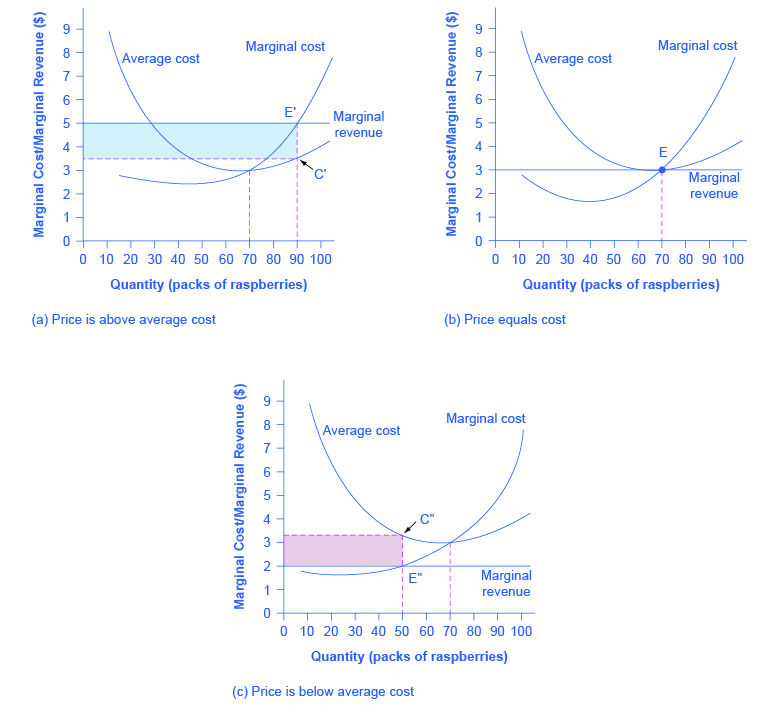

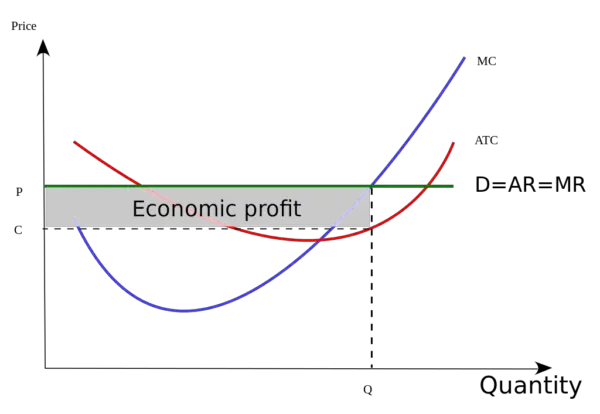

Since price is constant marginal revenue is also constant. Price ar mr. When ar and mr are parallel to x axis. Profit is equal to revenue less cost.

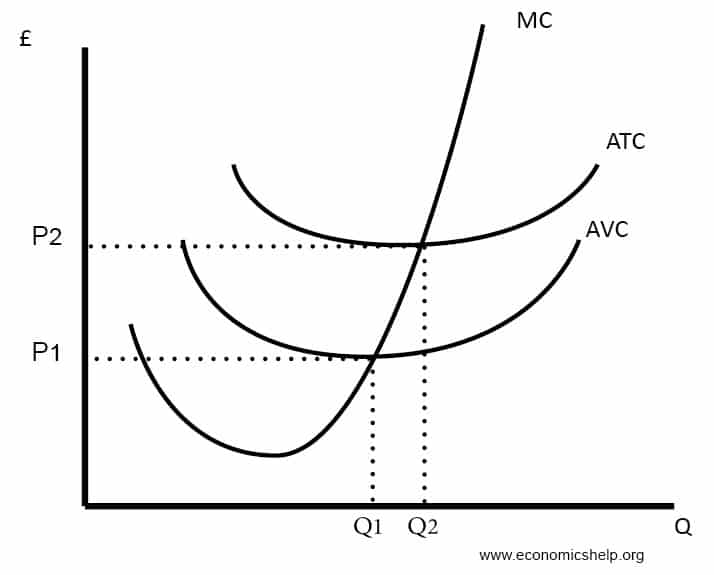

When production is 3 units marginal cost is less than the average cost. Total revenue minus the explicit cost of producing goods and services. Since price is constant marginal revenue equals price or average revenue. Because profit maximization happens at the quantity where marginal revenue equals marginal cost it s important not only to understand how to calculate marginal revenue but also how to represent it graphically.

This is clear from the above table. If average revenue and marginal revenue are parallel to horizontal axis then it means both ar and mr are equal to each other i e. Revenue is the income earned by a firm by the sale of goods and services. Marginal revenue minus marginal cost.

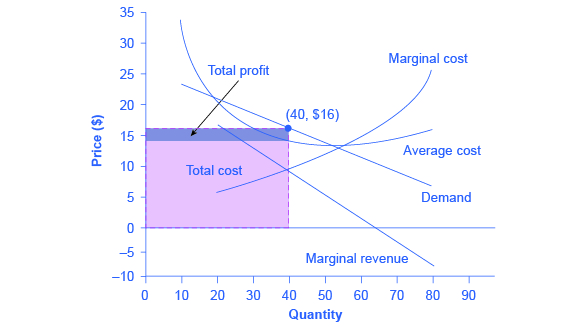

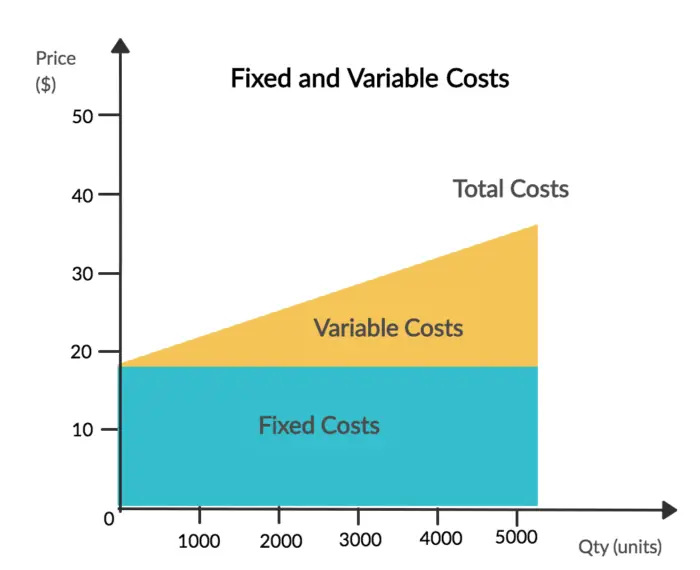

For example average cost ac also called average total cost is the total cost divided by quantity produced. Revenue denotes the amount of income which a firm receives by the sale of its output. Total revenue increases at a constant rate as additional units are produced and sold. Under such conditions the company will have no earnings left after paying its workers and suppliers and financing other overhead expenses such as rent of its stores research and.

Marginal cost mc is the incremental cost of the last unit produced. When on the other hand. Here we shall discuss the total revenue average revenue and marginal revenue. The average cost and marginal costs are calculated from total cost.

Cost refers to the expenses incurred by a producer for the production of a commodity. Revenue is different from profit. Average revenue minus the average cost of producing the last unit of a good or service. If average cost includes all costs as opposed to only variable costs the firm will neither make any money nor record a loss when average cost equals average revenue.

Total revenue minus the opportunity cost of producing goods and services. Indicated by the same horizontal line. Marginal revenue is the additional revenue that a producer receives from selling one more unit of the good that he produces. There are several ways to measure the costs of production and some of these costs are related in interesting ways.

Costs Of Production In A Perfectly Competitive Market Maple Programming Help

1

Pin On Economics

Relation Between Average Marginal And Total Cost Production Microeconomics

Unregulated Free Enterprise

Pin On All Academic Assignments Found Here

Types Of Costs Economics Help

Marginal Cost Definition Formula And 3 Examples Boycewire

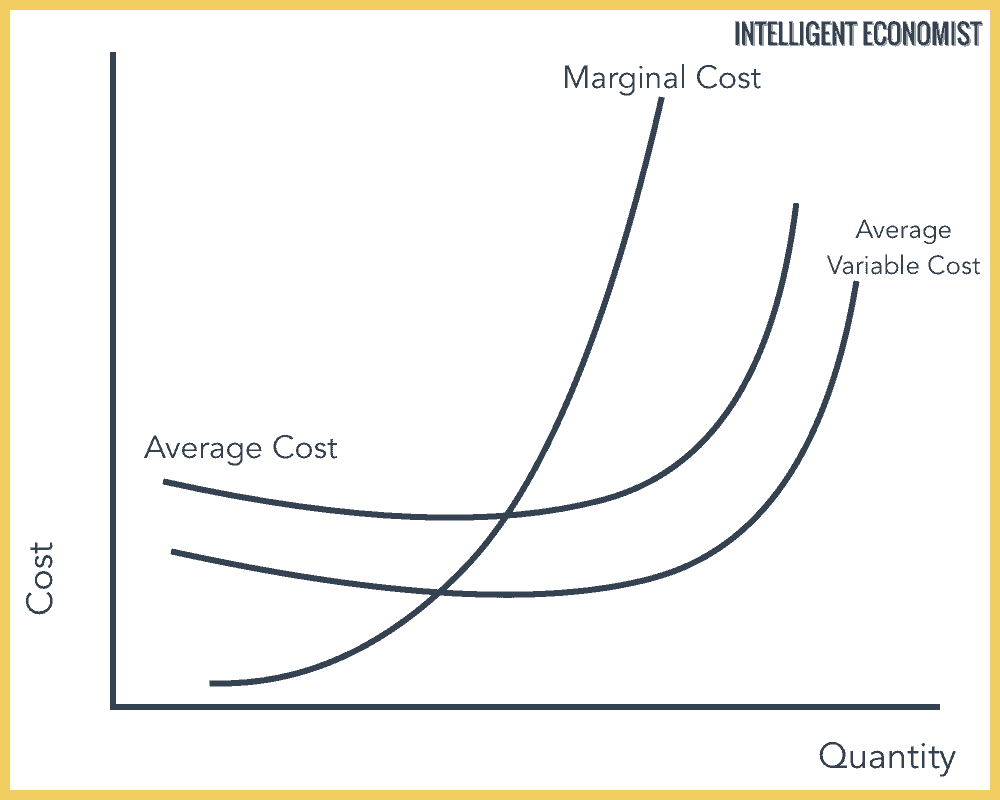

Theory Of Production Cost Theory Intelligent Economist

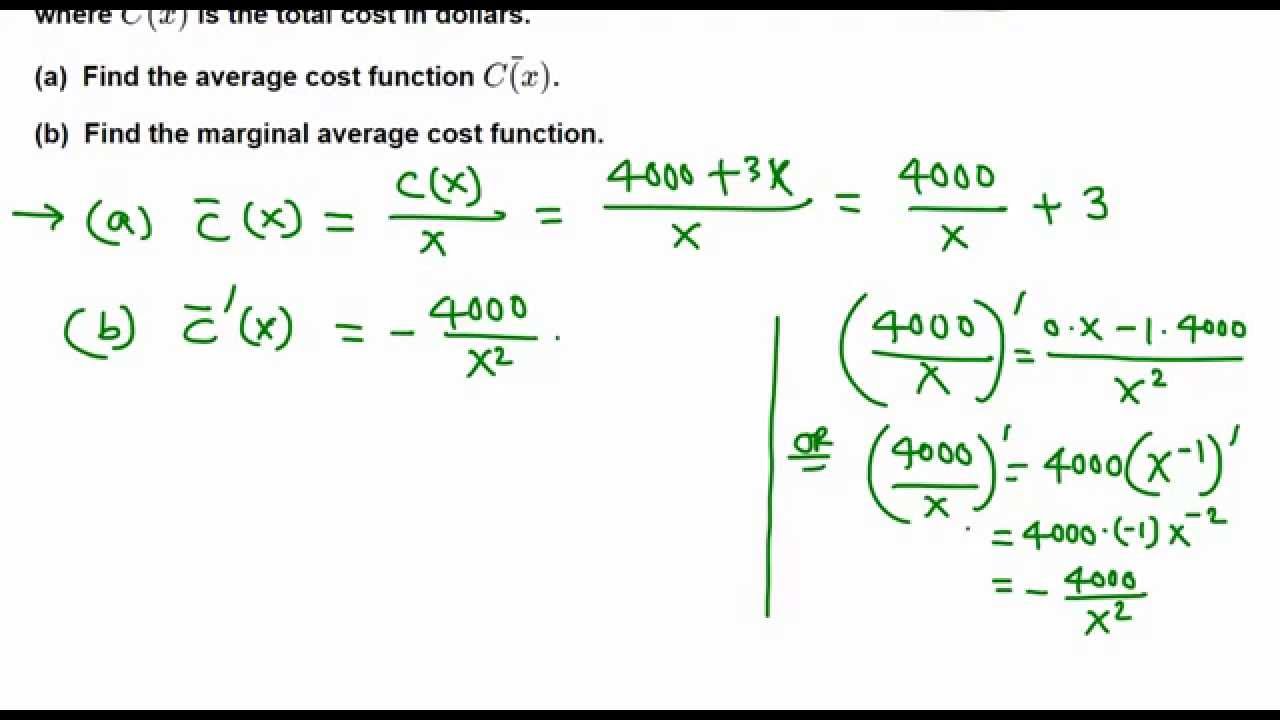

Marginal Average Cost Function Youtube

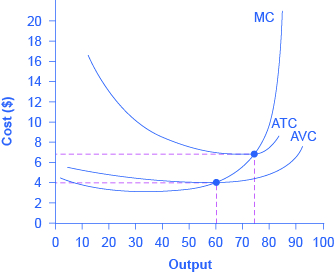

7 2 The Structure Of Costs In The Short Run Principles Of Economics

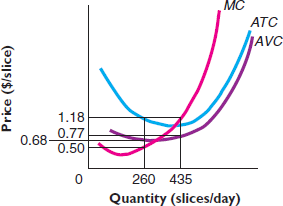

Solved For The Pizza Seller Whose Marginal Average Variable Chegg Com

Solved When Marginal Revenue Equals Marginal Cost A Pro Chegg Com