Revenue Is Always Recognized When Which Of The Following Occurs

Revenue Recognition Examples Know When Revenue Is Recorded

Revenue Recognition Boundless Accounting

F3 You Ll Remember Quizlet

:max_bytes(150000):strip_icc()/ScreenShot2020-10-27at3.34.43PM-253260b7e64f402aa5b3951a5d781292.png)

Unearned Revenue Definition

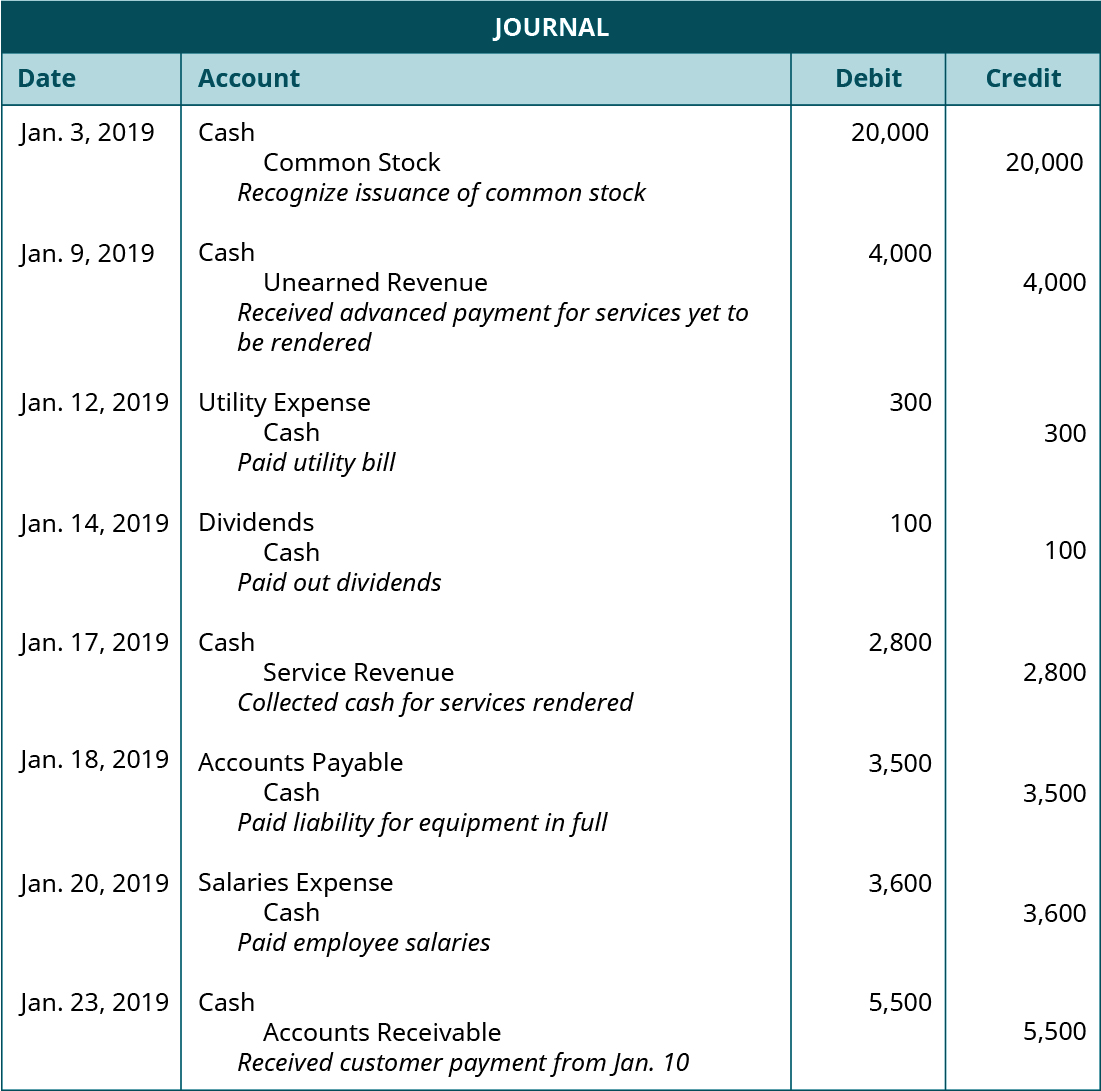

Use Journal Entries To Record Transactions And Post To T Accounts Principles Of Accounting Volume 1 Financial Accounting

Pdf Accounting For Adjusting Entries Key Terms And Concepts To Know Arif Mulyana Academia Edu

This guide addresses recognition principles for both ifrs and u s.

Revenue is always recognized when which of the following occurs. C complete information on the part of buyers and sellers. In an accrual based accounting revenue is recognized when it is earned. A a great number of buyers. Which of the following best represents the matching principle criteria.

Revenue is recognized in the period in which the performance obligation is satisfied. Changes in estimated variable consideration should be recognized as an adjustment to revenue in the period the change in estimate is made. Revenue always is recognized once the buyer has physical possession of goods. Which of the following is correct about changes in estimated variable consideration.

B easy entry into and easy exit from the market. The perfectly competitive model assumes all of the following except. Ias 18 outlines the accounting requirements for when to recognise revenue from the sale of goods rendering of services and for interest royalties and dividends. D that firms attempt to maximize their total revenue.

Revenue is measured at the fair value of the consideration received or receivable and recognised when prescribed conditions are met which depend on the nature of the revenue. Revenue is recognized when an order occurs and not when the actual sale is initiated. So the answer is none of the above unless the question was implying a cash or accrual bases accounting. According to the principle revenues are recognized when they are realized or realizable and are earned usually when goods are transferred or services rendered no matter when cash is received.

Revenue recognition is an accounting principle that outlines the specific conditions under which revenue is recognized. B revenue is recognized when goods are transferred to the consignee. A revenue is recognized at the point in time when the consignment arrangement is made. Revenue is recorded only when cash is received and expenses are recorded only when cash is paid.

False sellers should recognize revenue over time for a long term contract in which the seller is receiving periodic payments for progress to date but may need to refund those payments in the event the contract is cancelled. C revenue is recognized upon sale by the consignee to an end customer. In a cash basis accounting revenue is recognized when cash is collected out of the choices. The accrual basis of accounting is in accordance with generally accepted accounting principles.

Ias 18 was reissued in december 1993 and is operative for. Revenue and expenses are matched based on when expenses are paid. In theory there is a wide range of potential points at which revenue can be recognized.

Https Www Harpercollege Edu Academic Support Tutoring Subjects Pdf Acc101 Chapter3new Pdf

Revenue Recognition Loyalty Points Reward Program Accounting

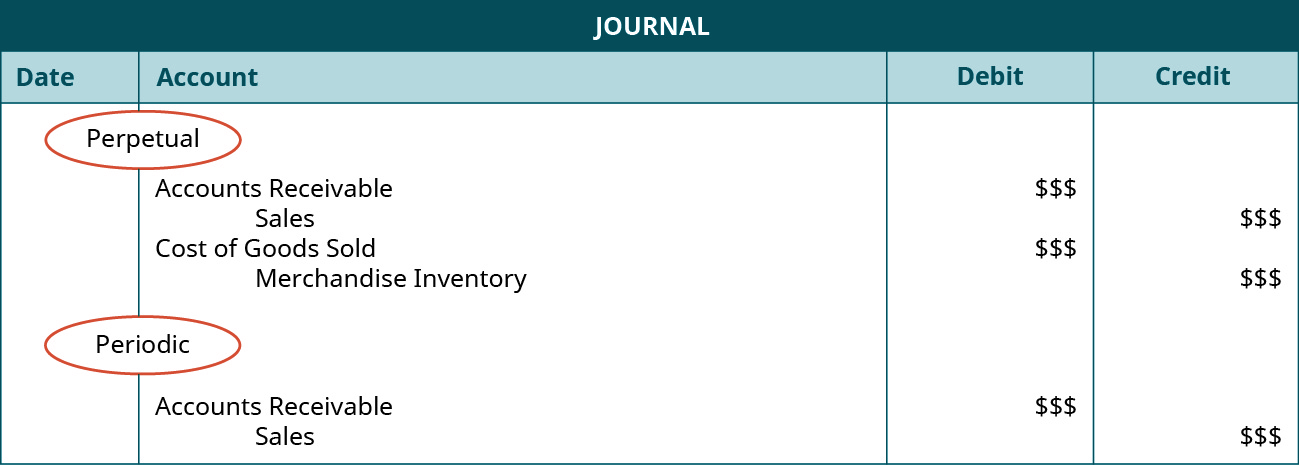

Compare And Contrast Perpetual Versus Periodic Inventory Systems Principles Of Accounting Volume 1 Financial Accounting

/dotdash_Final_Capital_Expenditures_vs_Revenue_Expenditures_Whats_the_Difference_2020-01-160a38c63f364966bfc46acc4b6b2917.jpg)

How Do Capital And Revenue Expenditures Differ

Significant Financing Component Revenue Recognition

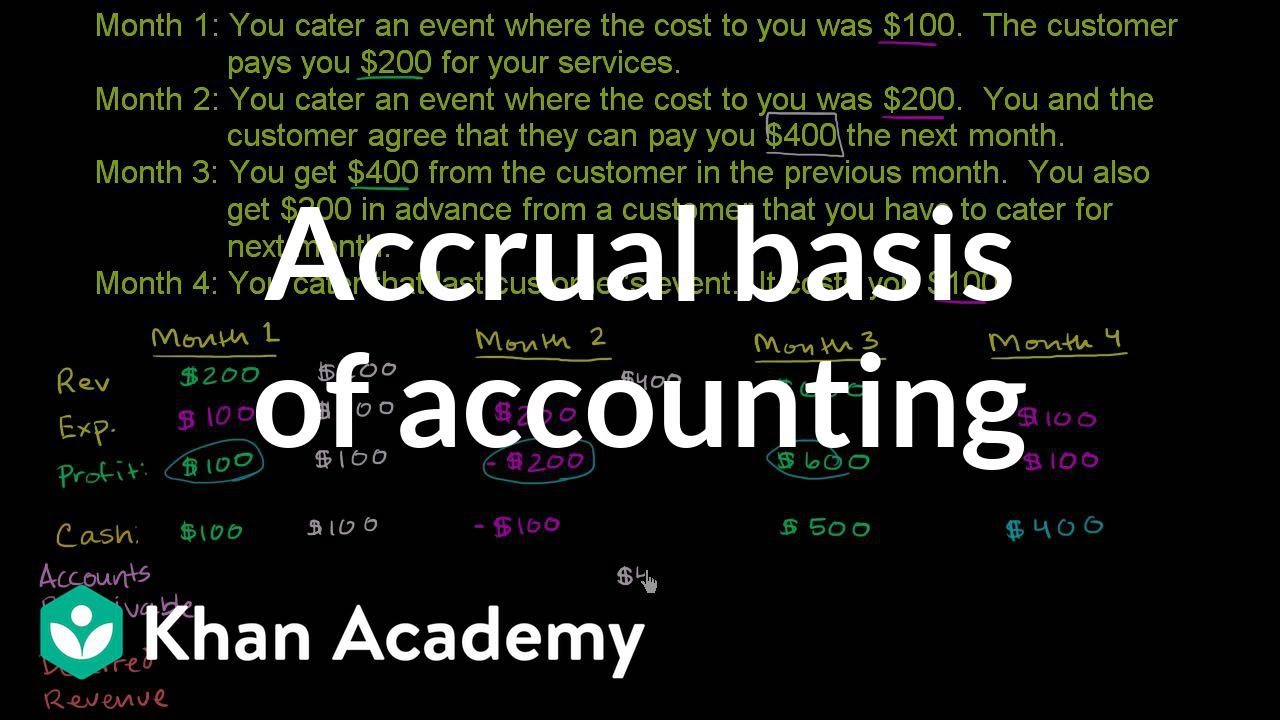

Accrual Basis Of Accounting Video Khan Academy

:max_bytes(150000):strip_icc()/dotdash_Final_What_Is_the_Difference_between_Revenue_and_Sales_Oct_2020-012-e50d6c289ebf4d00987fbae938815fd4.jpg)

How Do Tangible And Intangible Assets Differ

/Total-Revenue-or-Sales-on-the-Income-Statement-58a8e2295f9b58a3c9323d57.jpg)

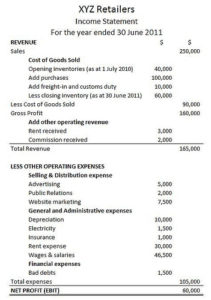

When Should A Company Recognize Revenues On Its Books

/GettyImages-1051929672-986f9246cdef4945889a2d1da90a6a57.jpg)

When Is Revenue Recognized Under Accrual Accounting

Completed Contract Methods Under Ifrs And Gaap Financial Statements Accounting In 2020 Financial Statement Method Contract

Accounting Input Vs Output Methods In Asc 606 Revenuehub

/dotdash_Final_How_Are_Prepaid_Expenses_Recorded_on_the_Income_Statement_Oct_2020-01-5994210f98a84b468a9a113c94643d50.jpg)

How Are Prepaid Expenses Recorded On The Income Statement