Revenue Is Generally Recognized When A Sale Occurs This Statement Describes The

Doc Chapter 2 Conceptual Framework Underlying Financial Accounting Huy Le Academia Edu

Explain The Revenue Recognition Principle And How It Relates To Current And Future Sales And Purchase Transactions Principles Of Accounting Volume 1 Financial Accounting

Revenue Recognition Boundless Accounting

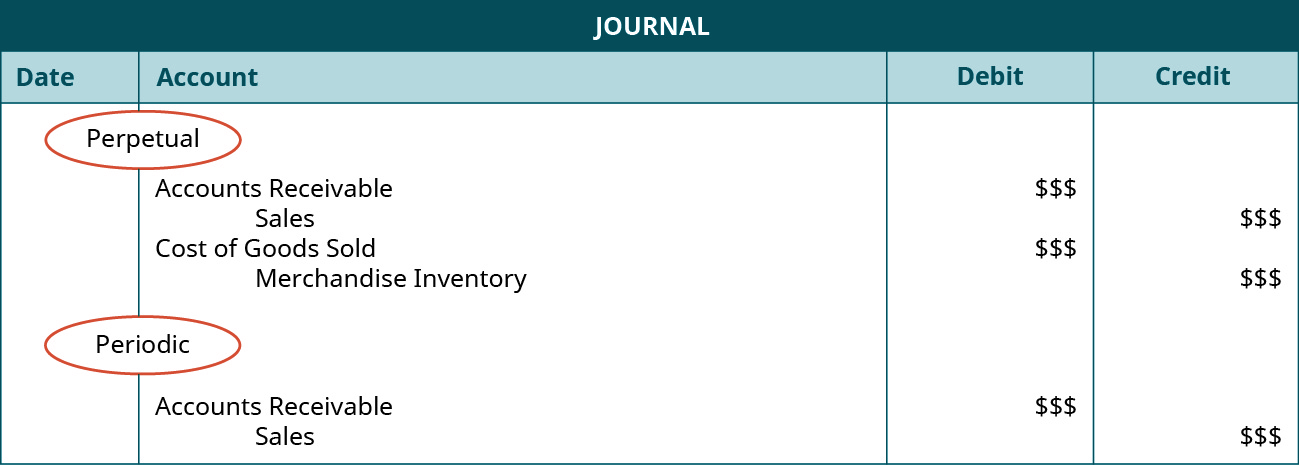

Compare And Contrast Perpetual Versus Periodic Inventory Systems Principles Of Accounting Volume 1 Financial Accounting

Define And Apply Accounting Treatment For Contingent Liabilities Principles Of Accounting Volume 1 Financial Accounting

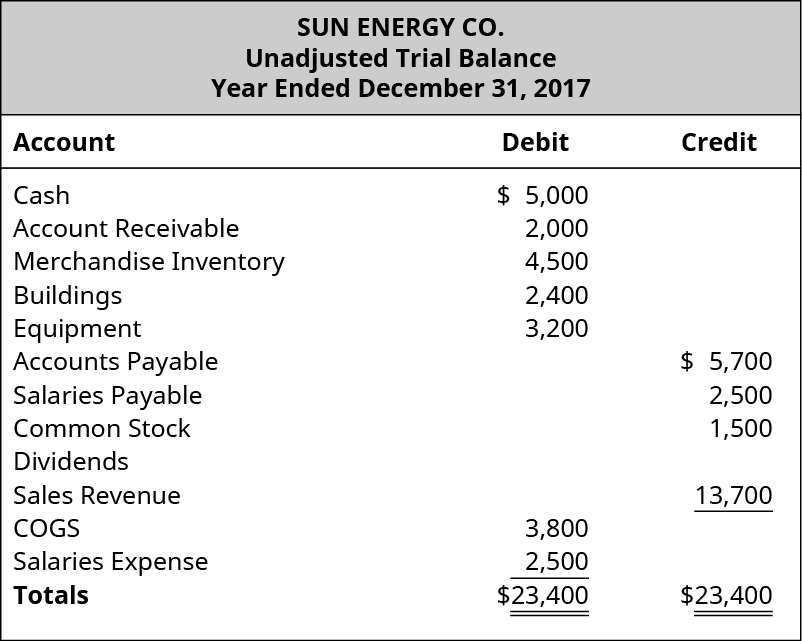

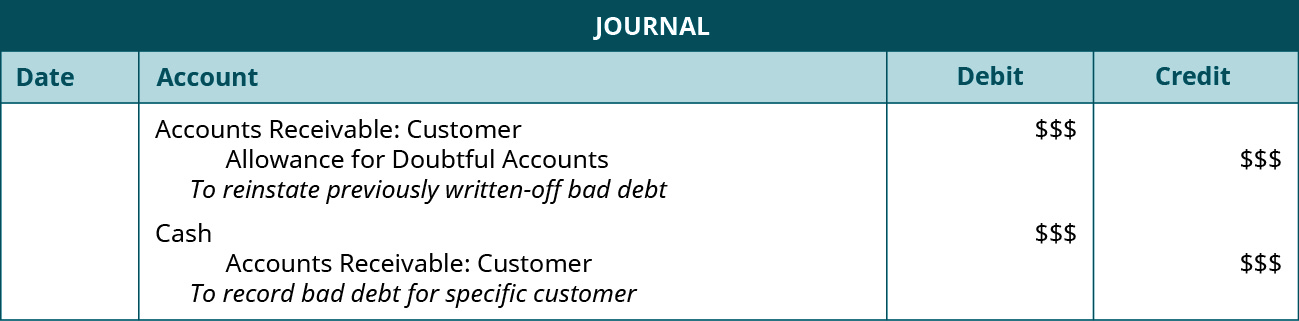

Account For Uncollectible Accounts Using The Balance Sheet And Income Statement Approaches Principles Of Accounting Volume 1 Financial Accounting

This statement describes the a.

Revenue is generally recognized when a sale occurs this statement describes the. Revenue recognition is an accounting principle that outlines the specific conditions under which revenue sales revenue sales revenue is the income received by a company from its sales of goods or the provision of services. Which of the following statements best describes the recognition of revenue. 3 in december 2019 swanstrom inc. Governments recognize revenues from exchange transactions when the cash is received and for nonexchange transactions when the resources are available to satisfy existing liabilities.

Generally revenue from sales should be recognized at a point when. Revenue recognition is a generally accepted accounting principle gaap that stipulates how and when revenue is to be recognized. This statement describes the a. The product is available for sale to the ultimate consumer.

Recognition occurs when the performance obligation is satisfied. Management decides it is appropriate to do so. According to generally accepted accounting principles for a company to record revenue on its books there must be a critical event to signal a transaction such as the sale of merchandise or a. On the date the sale is made b.

Revenue is recognized in the accounting period in which the performance obligation is satisfied. When transfer of ownership of goods sold is not immediate and delivery of the goods is required the shipping terms of the sale dictate when revenue is recognized. Receives a cash payment of 3 500 for services performed in december 2019 and a cash payment of 4 500 for services to be performed in january 2020. The installment sales method is used for tax purposes but the accrual method of recognizing sales revenue is used for financial reporting purposes.

The revenue recognition principle using accrual accounting. An example of a deductible temporary difference occurs when a. On the date the customer pays for the merchandise c. Accelerated depreciation is used for tax purposes but straight line depreciation is used for accounting purposes.

Either on the date when the sale occurs or the date on which the customer pays. The key elements of accrual basis accounting are the revenue recognition principle the expense recognition principle and the historical cost principle. Using the accrual basis of accounting when is revenue from the sale of merchandise normally recognized.

Distinguish Between Financial And Managerial Accounting Principles Of Accounting Volume 2 Managerial Accounting

Describe And Demonstrate The Basic Inventory Valuation Methods And Their Cost Flow Assumptions Principles Of Accounting Volume 1 Financial Accounting

:max_bytes(150000):strip_icc()/ScreenShot2020-10-27at3.34.43PM-253260b7e64f402aa5b3951a5d781292.png)

Unearned Revenue Definition

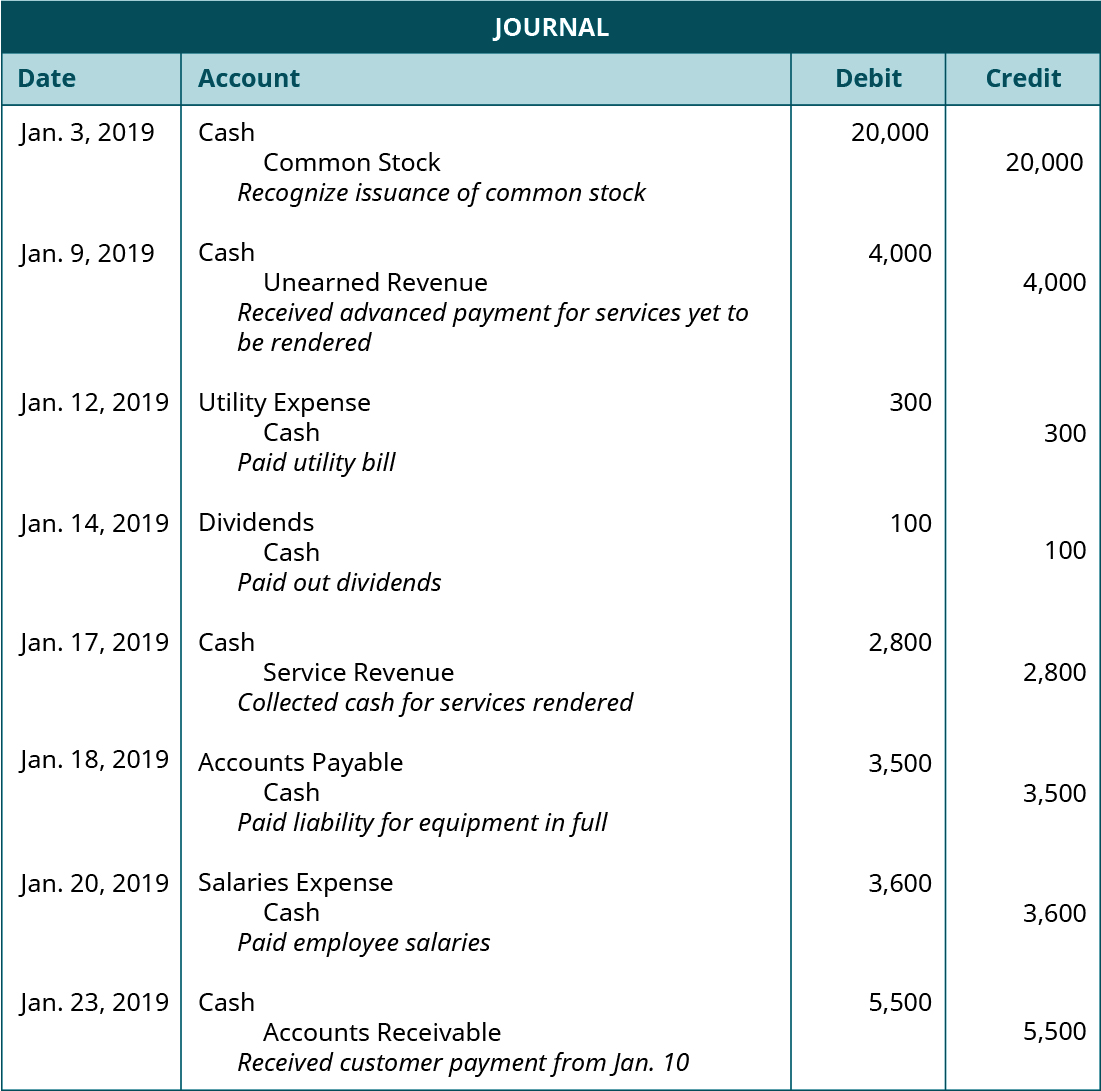

Use Journal Entries To Record Transactions And Post To T Accounts Principles Of Accounting Volume 1 Financial Accounting

Conveying Accounting Information Boundless Accounting

Best 4 Conceptual Framework Elements Of Financial Statements Flashcards Quizlet

Explain The Concepts And Guidelines Affecting Adjusting Entries Principles Of Accounting Volume 1 Financial Accounting

50wc Ztqzkccym

:max_bytes(150000):strip_icc()/dotdash_Final_What_Is_the_Difference_between_Revenue_and_Sales_Oct_2020-012-e50d6c289ebf4d00987fbae938815fd4.jpg)

How Do Tangible And Intangible Assets Differ

The Statement Of Cash Flows Boundless Accounting

The Accounting Concept Boundless Accounting

:max_bytes(150000):strip_icc()/T-Account2_2-88f09021aae149ca8fce870a08ae2752.png)

T Account Definition

Https Www Aicpa Org Research Standards Auditattest Downloadabledocuments Au C 00315 Pdf