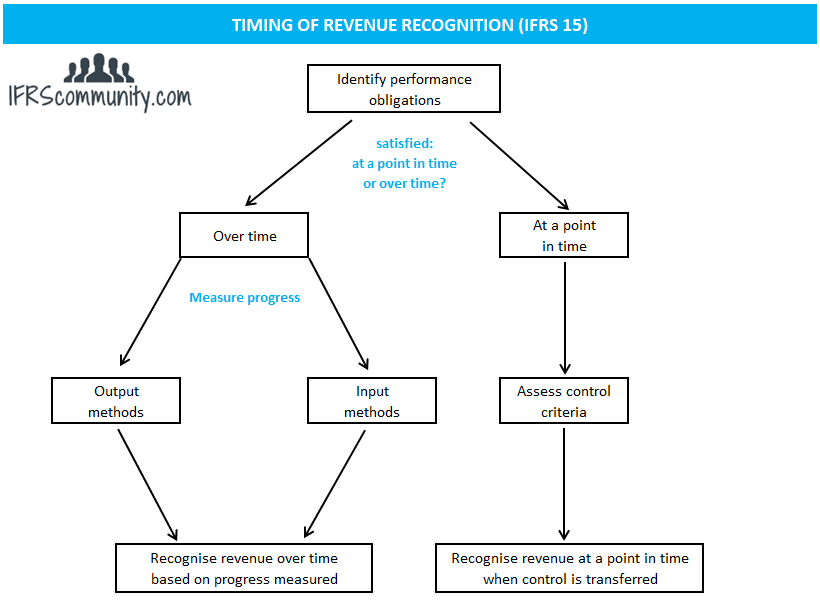

Revenue Is Recognized Over Time If The Buyer Effectively Controls The Asset As It Is Being Built

Performance Obligations And Revenue Recognition Ifrs 15 Ifrscommunity Com

An Analysis Of The New Sale And Leaseback Guidance The Cpa Journal

Understanding Non Controlling Interests Ncis Financial Edge Training

Https Www Ifrs Org Media Feature Meetings 2017 November Ifrs Ic Agenda Papers Ap2b Right To Payment For Performance Completed To Date Pdf

Accounting For Decommissioning Restoration And Similar Provisions To Make Good Rmg 114 Department Of Finance

Https Www Pwc Com Gx En Audit Services Ifrs Publications Ifrs 15 Pwc Revenue From Contracts With Customers Pharma Pdf

A share purchase requires the purchase of 100 percent of the shares of a company effectively transferring all of the company s assets and liabilities to the purchaser.

Revenue is recognized over time if the buyer effectively controls the asset as it is being built. The company s performance creates or enhances an asset and that the customer controls as the asset is created or enhanced. There are two core methods to buy or sell a business. Revenue is recognized when the buyer obtains control of the product. Ias 18 was reissued in december 1993 and is operative for.

Assets are listed on the balance sheet and revenue is shown on a company s income statement. Revenues are realized or realizable when a company exchanges goods or services for cash or other assets. Ias 18 outlines the accounting requirements for when to recognise revenue from the sale of goods rendering of services and for interest royalties and dividends. An asset purchase or a share purchase.

Revenue is not recognized under the realization principle unless the earnings process is complete or virtually complete and there is. Here s the full explanation of what assets and revenue are and. According to the principle revenues are recognized when they are realized or realizable and are earned usually when goods are transferred or services rendered no matter when cash is received. The seller is likely to do which of the following with respect to the time value of money over the life of the.

An asset purchase requires the sale of individual assets. Revenue from disposing of assets other than products is recognized at the date of sale. This is a key concept in the accrual basis of accounting because revenue can be recorded without actually being received. Long term construction contracts may be recognized over time.

Revenue from services rendered is recognized when cash is received or when services have been performed. Companies recognize revenue over a period of time if the customer receives and consumes the benefits as the seller performs and one of the following two criteria is met. Most revenue transactions pose few problems for revenue recognition because often the transaction is initiated and completed at the same time. The differences only grow from there.

Revenue is measured at the fair value of the consideration received or receivable and recognised when prescribed conditions are met which depend on the nature of the revenue. The seller is not enhancing an asset that the buyer controls or that has an alternative. Revenue should be recorded when the business has earned the revenue. Revenue is recognized over time.

The customer controls the asset as it is created or the company has no other use for the asset and 2.

Chapter 5 Flashcards Questions And Answers Quizlet

Licenses For Intellectual Property Revenuehub

Accounting For Sale And Leaseback Transactions Journal Of Accountancy

Https Www Bdo Com Getattachment 4495d805 F6c5 4eb5 8ade C3b59be821af Attachment Aspx

Chapter 20 Questions Answers

Https Www Cambridge Org Is Download File 968575 134388

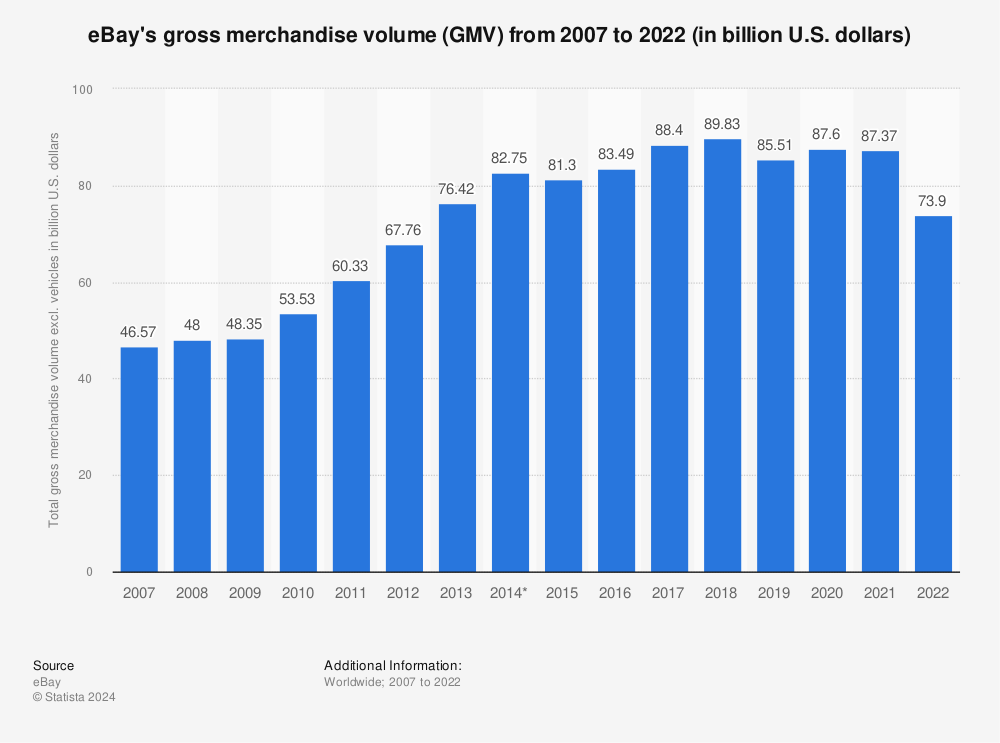

Ebay Case Study Smart Insights

/ExxonLongtermAssets2018-5c5485414cedfd0001efdb2c.jpg)

Long Term Assets Definition

:max_bytes(150000):strip_icc()/dotdash_Final_Why_Do_Bitcoins_Have_Value_Apr_2020-01-0a8036d672c34d69bd2f4f5175b754bb.jpg)

Why Do Bitcoins Have Value

:max_bytes(150000):strip_icc()/dotdash_Final_What_Is_the_Difference_between_Revenue_and_Sales_Oct_2020-012-e50d6c289ebf4d00987fbae938815fd4.jpg)

How Do Tangible And Intangible Assets Differ

Derivative Financial Instrument An Overview Sciencedirect Topics

Https Www Mossadams Com Getmedia 7a085f60 1924 4076 Ac91 Bc2a2828056b Lease Accounting Guide Pdf Ext Pdf