Total Sales Revenue Minus Total Variable Expenses

What Is The Difference Between Revenue And Profit Quora Ingles

Customizing You To Your Market Statement Template Profit And Loss Statement Income Statement

Pin On Accounting

Break Even Point In Dollars Form Good Essay Small Business Start Up Sample Resume

Inventory Turnover Inventory Turnover Cpa Exam Things To Sell

Stable Management Expenses Typical Horse Business Expenses Horse Barns Horse Stables Horse Farm Ideas

Describes how a cost changes as volume changes.

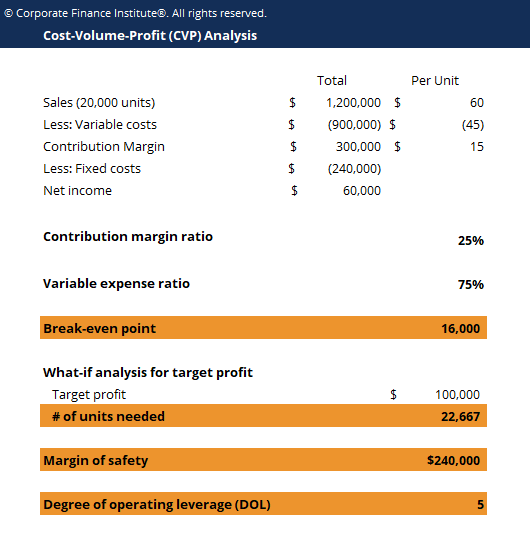

Total sales revenue minus total variable expenses. Costs that change in total in direct proportion to changes in volume. Your total racket sales are 150 and your total revenues are 6 500. If you sell 50 tennis rackets for 70 dollars each your total revenue for those sales is 3 500. By excluding all fixed costs the content of the cost of goods sold figure now changes to the.

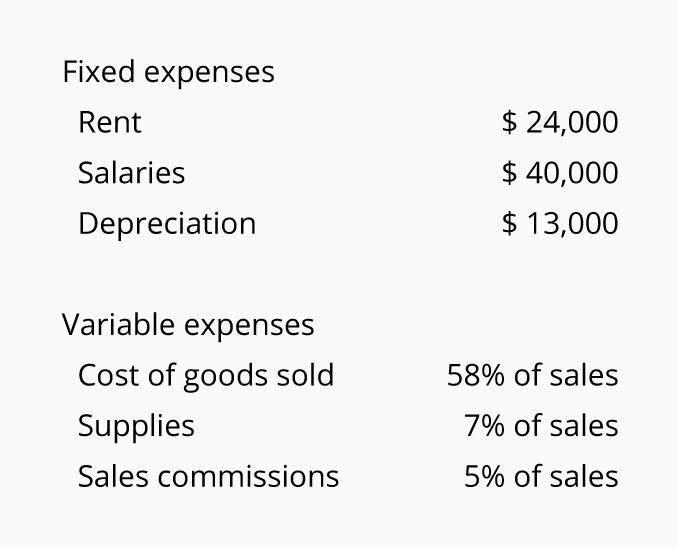

The band of volume where total fixed costs and variable cost per unit remain constant. Here we are given all the variable cost per unit and therefore we can use the below formula to calculate the total variable cost per unit. The operating income that results when sales revenue minus variable and minus fixed costs equals management s profit goal. Variable cost per unit highest cost lowest cost highest volume.

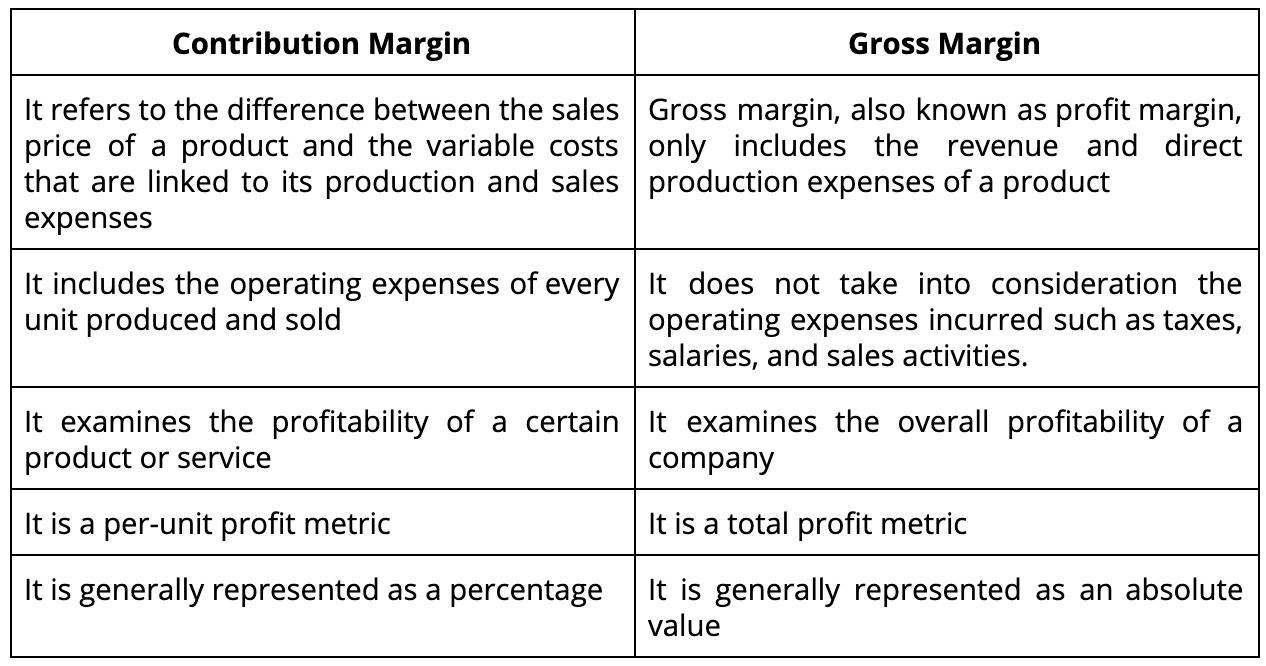

Variable costs are costs which change with a change in output for example cost of raw materials direct labor variable manufacturing overheads etc. This can be increased by increasing the price decreasing the costs while keeping the price constant and or increasing the sales. Variable overhead costs such as production supplies fixed overhead costs such as equipment depreciation and supervisory salaries an alternative to the gross margin concept is contribution margin which is revenues minus all variable costs of sales. It equals total variable costs divided by total sales or variable cost per unit divided by price per unit or 1 minus contribution margin ratio.

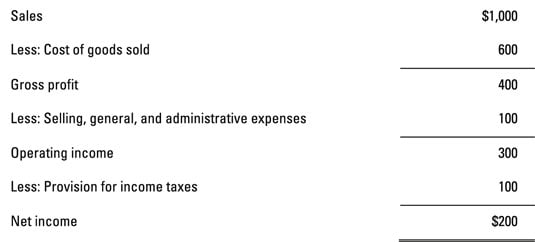

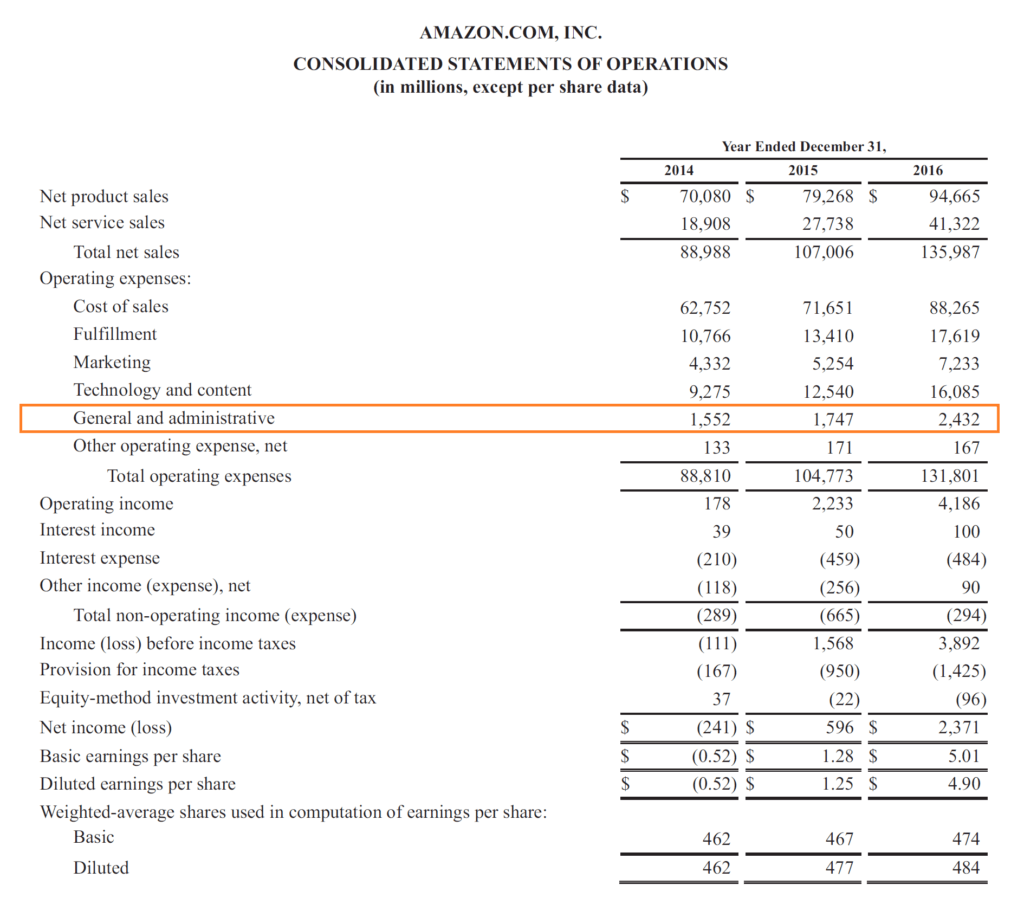

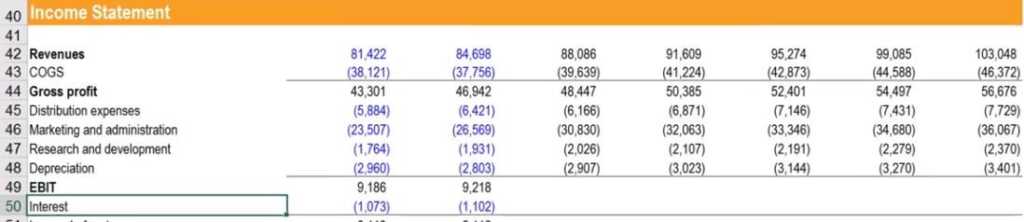

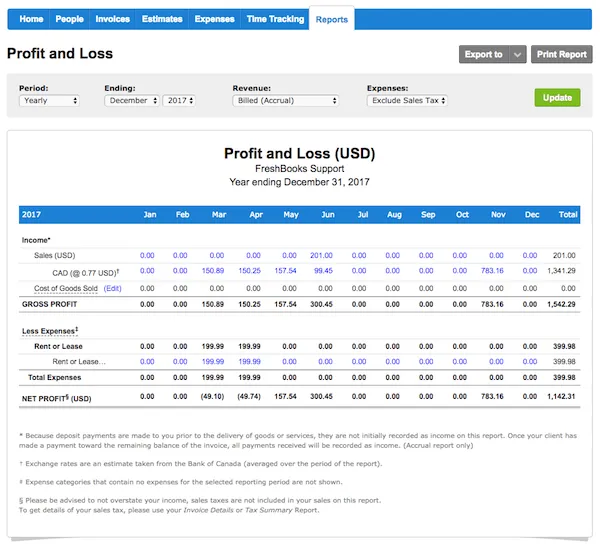

Contribution margin refers to sales revenue minus total variable costs. Revenues are the monies you generate from sales or other activities. Gross profit will appear on a company s income statement and can be calculated by subtracting the cost of goods sold from revenue sales. Therefore the calculation will be as follows.

For example if you sell 100 tennis rackets at 30 each your total revenue from those racket sales is 3 000. It is the amount available to cover fixed costs to be able to generate profits. The concept of contribution margin is fundamental in cvp analysis and other management accounting topics. These figures can be found on a company s income statement.

You are to calculate the total variable cost of the product x. Net sales revenue per unit variable cost per unit. The total number of units produced was 1 000 units. Costs that do not change over wide ranges in volume.

Margin Of Safety Formula Guide To Performing Breakeven Analysis

How To Compute Contribution Margin Dummies

/TeslaQ2-19IncomeStatementInvestopedia-1466e66b056d48e6b1340bd5cae64602.jpg)

Does Gross Profit Include Labor And Overhead

Break Even Point Quiz And Test Accountingcoach

Answered Determine The Amount Of Sales Units Bartleby

Cvp Analysis Guide How To Perform Cost Volume Profit Analysis

Prepare Operating Budgets Principles Of Accounting Volume 2 Managerial Accounting

:max_bytes(150000):strip_icc()/Apple10KIS-00e74dfe3f34479180ac7ede7b982292.jpg)

Return On Revenue Ror Definition

What Is Contribution Margin

Sg A Expense Selling General Administrative Guide Examples

Financial Forecasting Guide Learn To Forecast Revenues Expenses

What Is Cost Of Goods Sold Cogs And How To Calculate It

What Is The Weighted Average Cost Method Explained