License Revenue Ifrs 15

Performance Obligations And Revenue Recognition Ifrs 15 Ifrscommunity Com

Ifrs 15 For The Tmt Industries Timing Of Revenue Recognition Licences Bdo Australia

Https Www Xrb Govt Nz Dmsdocument 726

Https Www Xrb Govt Nz Dmsdocument 3177

Https Www Bdo Nz Getmedia 001ebe9d 9dfa 4d55 A93e 67642e554ab7 Bdo Nz Ifrs 15 Software Aspx

Https Www Xrb Govt Nz Dmsdocument 881

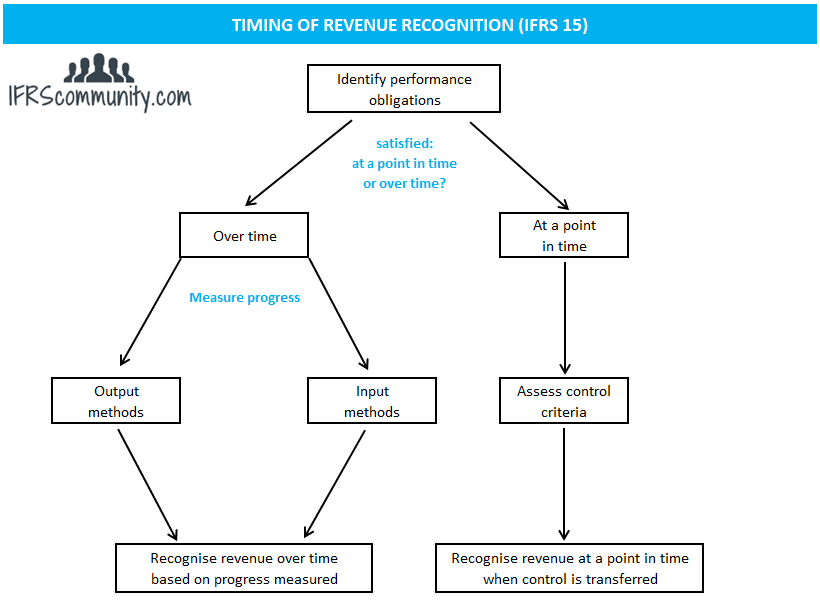

Here ifrs 15 provides the specific guidance for the licenses but only if the license is distinct.

License revenue ifrs 15. It says that you can sell two types of licenses. Syngenta recognizes that revenue on signature of or on the effective date of the license whichever is later. The issuance of ifrs 15 revenue from contracts with customers by the iasb has required r c preparers to consider all of their revenue and promotion models using the new five step model detailed in the standard. If the criteria from ifrs 15 b58 listed above are not met the performance obligation is satisfied at a point in time at which the licence is granted to the customer.

Under ifrs 15 the pattern of revenue recognition could therefore change for many tmt entities particularly with regard to licence contracts. Sales of software are frequently in the form of a licence to use the software. Common examples on transition 3 1. Ifrs 15 specifies how and when an ifrs reporter will recognise revenue as well as requiring such entities to provide users of financial statements with more informative relevant disclosures.

Example 1 change in timing of revenue recognition example 1 a vendor a music record label licenses a specified recording of a beethoven symphony to a customer from 1 march 2017 to 28 february 2018. Revenue is recognised when as performance obligations are satisfied in the amount of transaction price allocated to satisfied performance obligations ifrs 15 46. When to recognise revenue. At the same time our old publication has been rendered obsolete.

Ifrs 15 includes specific guidance for licensing arrangements. 8 ifrs in practice 2019 fi ifrs 15 revenue from contracts with customers transition 3. Syngenta early adopted ifrs 15 revenue from contracts with customers with effect. The standard provides a single principles based five step model to be applied to all contracts with customers.

A performance obligation is satisfied by transferring a promised good or service to a customer ifrs 15 31. Ifrs 15 was issued in may 2014 and applies to an annual reporting period beginning on or.

Https Www Pwc Com Gx En Services Audit Assurance Assets Ifrs 15 For The Software Industry In Brief Pdf

Revenue From Licensing Of Intellectual Property Ifrs 15 Ifrscommunity Com

Defining Issues 15 21 Fasb Proposes Clarifications To License And Performance Obligation Guidance For Revenue With Images Finance Financial Asset Financial Statement

Contract Assets And Contract Liabilities Ifrs 15 Ifrscommunity Com

Xiaomi S Q3 Report Profit Growing Despite A Slight Decline In Smartphone Sales Fortune Global 500 Marketing Set Net Income

Https Www Pwc Com Gx En Audit Services Ifrs Publications Ifrs 15 Ifrs 15 In Brief Iasb Issues Amendment Pdf

Understanding Revenue Recognition For Subscription Businesses Cerillion

Https Www Ifrs Org Media Feature News 2019 June Basics Of New Ifrs Standards And Research Eaa Paphos Pdf

Https Www Pwc Com Gx En Audit Services Ifrs Publications Ifrs 15 Pwc Revenue From Contracts With Customers Entertainment And Media Pdf

Ifrs 15 Revenue From Contracts With Customers

Ifrs 15 Revenue From Contracts With Customers Acca Sbr Got It Pass

Simplify Compliance With The New Ifrs 15 Revenue Recognition Standard Dxc Technology

Revenue Recognition Standard Point Of Time Or Period Of Time Insights Blum